Every dollar spent on marketing should bring in customers — but most businesses have no clear idea how much each new customer actually costs to acquire. Customer acquisition cost, commonly abbreviated as CAC, is the metric that answers that question precisely. It measures the average amount your business spends across all marketing and sales activities to win a single paying customer during a defined time period.

Knowing your CAC is not just a reporting exercise. It shapes budget decisions, channel strategy, pricing models, and how quickly you can scale without burning through cash. Whether you run a startup, an e-commerce store, or a B2B SaaS company, understanding CAC gives you a direct read on marketing efficiency. This article breaks down the standard CAC formula, walks through simple and channel-level calculation examples, highlights the most common mistakes, and explains how to put the number to work once you have it.

What Customer Acquisition Cost Means for Marketing Performance

Customer acquisition cost is a measure of spending efficiency. It tells you, on average, how much investment is required to convert a prospect into a paying customer. Businesses track CAC because it directly connects the money going out — on ads, sales staff, tools, and content — to the revenue coming in from new customers.

A low CAC relative to what customers are worth to the business signals efficient growth. A high CAC is not automatically a problem, but it must be supported by customers who spend enough over time to justify the cost. This is why CAC is almost always discussed alongside customer lifetime value — the two numbers together reveal whether growth is sustainable.

Why Businesses Track CAC

- Budget allocation: CAC broken down by channel shows where spend is most efficient, making it easier to shift investment toward top-performing sources.

- Leadership and investor reporting: CAC is a standard benchmark for evaluating business model health, especially in venture-backed growth companies.

- Pricing and margin decisions: If acquisition cost exceeds what a customer pays, the unit economics are broken regardless of revenue growth.

- Efficiency benchmarking over time: Tracking CAC month over month reveals whether marketing is improving or deteriorating in how well it converts spend into customers.

Who Should Measure CAC

Any business that spends money to attract customers should measure CAC. It is especially critical in paid advertising, subscription models, SaaS products, and e-commerce, where acquisition spend is high and customer value can be tracked over time. Even service businesses and agencies benefit from knowing CAC when justifying internal headcount or demonstrating efficiency to clients.

The CAC Formula and What to Include in the Calculation

The core CAC formula is straightforward:

CAC = Total Acquisition Costs ÷ Number of New Customers Acquired

The challenge is not the formula itself — it is deciding what goes into total acquisition costs. Many businesses undercount these costs, which produces an optimistically low CAC that does not reflect how much the business is actually spending to grow.

What to Include in Total Acquisition Costs

- Paid advertising spend: Google Ads, Meta Ads, LinkedIn, programmatic display, and any other paid channel budget.

- Marketing team salaries and contractor fees: The people managing campaigns, writing content, running paid channels, and producing creative assets.

- Marketing software and tools: CRM subscriptions, email platforms, analytics tools, SEO software, and automation systems.

- Sales team costs: When sales reps are involved in closing new customers, their salaries, commissions, and related overhead belong in the acquisition cost.

- Creative production: Photography, video production, design, copywriting, and landing page development.

- Agency and freelancer fees: Any external support engaged specifically to acquire or convert customers.

- Events and sponsorships: Trade shows, webinars, or sponsorship deals intended to generate new customer relationships.

What to Exclude

Costs tied to serving existing customers — such as customer success salaries, onboarding resources, or product support teams — should generally be excluded. The goal is to isolate what you spend to bring someone in, not to keep them. Some advanced models separate sales costs from marketing costs to produce a pure marketing CAC and a blended total CAC for different analytical purposes.

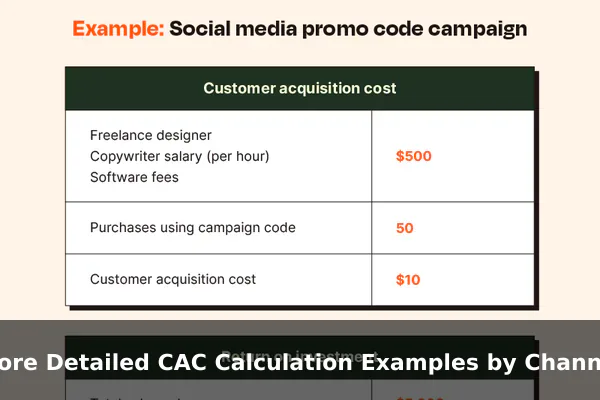

Simple CAC Formula Example

Here is a straightforward example using a single monthly period for a SaaS company.

The company spends the following in one calendar month:

- Paid advertising: $8,000

- Marketing team salaries, acquisition-allocated portion: $5,000

- Sales team costs: $4,000

- Tools and software subscriptions: $1,000

Total acquisition costs: $18,000

During that same month, the company gained 60 new paying customers.

Applying the CAC formula:

CAC = $18,000 ÷ 60 = $300 per customer

This means the company spends an average of $300 to acquire each new customer. Whether $300 is efficient depends on what those customers are worth. If the average customer pays $50 per month and remains for 18 months, their lifetime value is $900 — making the $300 CAC look very reasonable at a 3:1 LTV-to-CAC ratio, which is widely considered a healthy benchmark for subscription businesses.

More Detailed CAC Calculation Examples by Channel

A blended CAC gives you a business-level view, but breaking the calculation down by acquisition channel is where actionable insight lives. Not all channels are equally efficient, and channel-level CAC reveals exactly which ones deliver customers at the best cost per acquisition.

Example: Paid Search CAC

A B2B software company runs Google Ads for one quarter with these costs:

- Ad spend: $12,000

- In-house PPC management, time allocation: $2,000

- Landing page design and testing: $500

- New paying customers from this channel: 25

Paid Search CAC = $14,500 ÷ 25 = $580

Example: Content Marketing CAC

The same company runs a content marketing program in parallel during the same quarter:

- Content writer salaries, quarterly portion: $6,000

- SEO tools and content distribution: $1,000

- New paying customers attributed to organic content: 40

Content Marketing CAC = $7,000 ÷ 40 = $175

Example: Email Outbound CAC

- Sales development rep salary portion: $4,000

- Email outreach software: $500

- New paying customers from outbound email: 10

Email Outbound CAC = $4,500 ÷ 10 = $450

Laid side by side, content marketing delivers the lowest CAC at $175 while paid search runs highest at $580. This does not mean the company should abandon paid search — speed to results, scalability, and lead quality all factor in — but the numbers give decision-makers a clear picture of where acquisition spend returns the most value per dollar.

Common CAC Mistakes That Skew the Numbers

Even experienced marketers introduce errors when calculating CAC. These mistakes produce misleading numbers that lead directly to poor budget and channel decisions.

Excluding People Costs

The most frequent error is calculating CAC using only ad spend while ignoring salaries, freelancer fees, and management time. A campaign spending $5,000 on ads that also requires 40 hours of team time at $50 per hour actually costs $7,000 — a 40% undercount if people costs are left out entirely.

Mixing Time Periods

Matching spend to customers acquired in the same period is essential. If you spend heavily on a campaign in October but most conversions happen in November or December, attributing those customers to October spend will make CAC look artificially high in one period and artificially low in another. For businesses with long conversion cycles, cohort-based attribution provides a more accurate picture.

Counting Leads Instead of Customers

CAC must always be calculated using actual paying customers, not leads, free trial users, or sign-ups. Conflating these inflates the denominator and creates a falsely low CAC number. A free trial user who never purchases is not a customer acquisition.

Ignoring Overhead and Software Costs

CRM platforms, analytics tools, and paid advertising software are real parts of what it costs to acquire customers. Excluding them causes systematic undercounting, particularly for teams that rely heavily on marketing technology stacks.

Using a Flawed Attribution Model

Multi-channel campaigns make attribution complex. Assigning 100% of a conversion to the last touchpoint may significantly undervalue top-of-funnel channels — such as content or social — that influenced the customer earlier in their journey. The choice of attribution model can substantially change what your per-channel CAC figures look like and how you respond to them.

How to Interpret CAC With LTV and Payback Period

CAC alone is not enough to make sound decisions. Two additional metrics give it the context it needs: customer lifetime value and the CAC payback period.

The LTV:CAC Ratio

LTV measures the total revenue a customer is expected to generate over the full length of their relationship with your business. The ratio of LTV to CAC is one of the most commonly used benchmarks for evaluating acquisition efficiency and business model health.

- LTV:CAC below 1:1 — You spend more acquiring customers than they return. This is unsustainable without a clear plan to change it.

- LTV:CAC of 1:1 to 2:1 — Margins are thin. Acquisition is not efficient enough to support long-term profitable growth.

- LTV:CAC of 3:1 — Generally considered healthy across many business models, particularly in subscription and SaaS contexts.

- LTV:CAC above 5:1 — May signal under-investment in growth. There may be room to spend more on acquisition while still generating strong returns.

The CAC Payback Period

The payback period measures how many months it takes to recover the cost of acquiring a customer through their monthly revenue contribution:

Payback Period = CAC ÷ Monthly Revenue per Customer

With a CAC of $300 and monthly revenue of $50 per customer, the payback period is 6 months. For subscription businesses, payback periods under 12 months are widely considered strong. Longer payback periods are acceptable when churn is very low and LTV is high — but they require more working capital to sustain aggressive growth.

Ways to Lower CAC Without Hurting Lead Quality

Reducing CAC is not simply about cutting ad budgets. The most durable improvements come from increasing conversion rates, refining targeting precision, and building systems where existing customers contribute to new customer acquisition.

Improve Landing Page Conversion Rate

If your current page converts at 2% and optimization brings it to 4%, you effectively halve your CAC without reducing a single dollar of ad spend. Better copy, clearer calls to action, stronger social proof, and systematic A/B testing are among the fastest levers available for lowering cost per acquired customer.

Tighten Audience Targeting

Broad targeting generates more impressions but frequently attracts prospects unlikely to convert. Narrowing your audience to higher-intent segments — even if it raises cost per click — typically lowers cost per actual customer acquired by reducing wasted spend on unqualified traffic.

Build Referral and Word-of-Mouth Systems

Customers who arrive through referral tend to cost far less to acquire and retain at higher rates. Structured referral programs and post-purchase experiences that generate organic word-of-mouth can meaningfully reduce blended CAC over time by increasing the proportion of near-zero-cost acquisitions.

Shorten the Sales Cycle

Longer sales cycles mean sales costs accumulate over more months before a customer converts. Improving lead qualification, streamlining the demo process, and providing better self-serve information can reduce the number of touchpoints needed to close, directly lowering the sales cost component of your CAC calculation.

When to Review CAC and What Benchmarks Really Mean

CAC should be reviewed at consistent intervals — monthly for businesses with high ad spend and short conversion cycles, quarterly for companies with longer sales cycles or primarily organic acquisition. Reviewing less frequently than quarterly risks missing deterioration until it has already meaningfully impacted margin or growth capacity.

How Industry Benchmarks Vary

Published CAC benchmarks differ significantly by business model, pricing tier, and market. A SaaS product at $400 per month can sustain a much higher CAC than a consumer brand selling a $60 item. Growth stage matters too: early-stage companies often accept elevated CAC intentionally while testing channels, trading short-term efficiency for channel-level learning.

Typical CAC ranges by business type for general orientation:

- E-commerce: $10–$100 for lower-priced products; $100–$500 for higher-ticket items

- SaaS serving small businesses: $100–$500

- SaaS serving enterprise accounts: $1,000–$10,000 or more, driven by long sales cycles and human-intensive closing

- Financial services: $200–$900

- Healthcare consumer products: $150–$400

The most meaningful benchmark is your own historical trend and whether your LTV justifies the current figure. Industry data provides orientation, not answers.

When a Rising CAC Is Acceptable

Not every increase in CAC is a warning sign. When a business enters a new market, tests an unfamiliar channel, or scales ad spend faster than it can optimize, CAC often rises temporarily. The key question is whether the increase is deliberate and time-bounded, or whether it reflects deteriorating efficiency with no corrective plan in place. Tracking CAC alongside conversion rate, payback period, and LTV provides the full picture needed to make that judgment with confidence.

Conclusion

Customer acquisition cost is one of the most actionable numbers in any marketing operation. When calculated correctly — with full costs included and aligned to the right time period — it tells you clearly how efficiently your business converts spend into customers. The CAC formula is simple: total acquisition costs divided by new customers acquired. The real work lies in gathering the right inputs, tracking the metric consistently, and interpreting it in relation to LTV and payback period rather than reading it in isolation.

Whether your CAC is $30 or $3,000, what matters most is the trend over time and how it compares to what customers are worth to your business. Use channel-level calculations to identify where acquisition spend is working hardest, avoid the common mistakes that distort the number, and pursue improvements that bring CAC down without sacrificing the quality of the customers you bring in.

{kind=link}